Three capital events this week. $75 billion priced. $35 billion closed. $6 billion stalled.

The first was the largest IPO in history. The second was the largest private credit tranche ever assembled in AI infrastructure. The third was a bilateral loan against the most valuable private AI company on earth that could not find a market. None of them ran through NVIDIA.

The centre of gravity hasn't moved.

The orbits around it just got wider.

I'm Ben Baldieri, and every week I break down the moves shaping GPU compute, AI infrastructure, and the data centres that power it all.

Here's what's inside this week:

Let's get into it.

Broadcom, Apollo, and Blackstone Build Anthropic a $35 Billion XPU Neocloud

The second non-NVIDIA neocloud built at hyperscaler scale in three issues.

Broadcom, Apollo, and Blackstone launched the AI XPV Platform on June 9: a financing vehicle targeting 20+ gigawatts through 2028 on Broadcom XPUs and networking. Apollo led the $35 billion initial tranche; Blackstone Credit & Insurance anchored. The capital funds Anthropic's 1GW+ expansion into Fluidstack sites from mid-2026, with capacity also designed for OpenAI through 2028.

Why this matters:

Blackstone is now backing two structurally separate non-GPU clouds: TPU with Meta and Google silicon (Issue #107), and XPU with Anthropic and Broadcom silicon. Combined committed capital tops $50 billion before either deploys a rack.

Anthropic now buys compute from every major silicon vendor: Google TPUs, Amazon Trainium, NVIDIA via Colossus (Issue #107), Microsoft Maia, Broadcom XPUs via Fluidstack. The $65B Series H (Issue #108) funded it.

Private credit and insurance balance sheets are now financing non-NVIDIA AI infrastructure at scale. IREN's A-rated GPU debt (Issue #109) opened that door for NVIDIA three months ago. Apollo walked through it at multiples of the size, for everything else.

SoftBank's $6 Billion OpenAI Margin Loan Stalls Weeks After Being Cut From $10 Billion

The largest single piece of friction in the AI capital flow this week.

Bloomberg reported on June 10 that SoftBank's talks to raise $6 billion via a margin loan backed by its OpenAI stake have stalled. $5 billion in soft commitments was secured before the pause, down from a $10 billion target cut 40% in May. A $40 billion bridge against the same position is due March 2027.

Why this matters:

Capital is moving aggressively into AI infrastructure at the institutional end: $35B Apollo and Blackstone, $4.25B Hut 8 (EE), $17.5B Amazon (EE). Meanwhile a $6B bilateral loan against the most valuable private AI company cannot find a market. The flows are concentrated and selective.

The creditor concern is OpenAI's private valuation. Without a public reference price, lenders cannot agree on what the collateral is worth.

SoftBank's AI commitments exceed $135 billion: OpenAI ($60B+), France (€75B, Issue #109), Ohio (Data Centre). The stalled loan is scepticism about that concentration, not about AI.

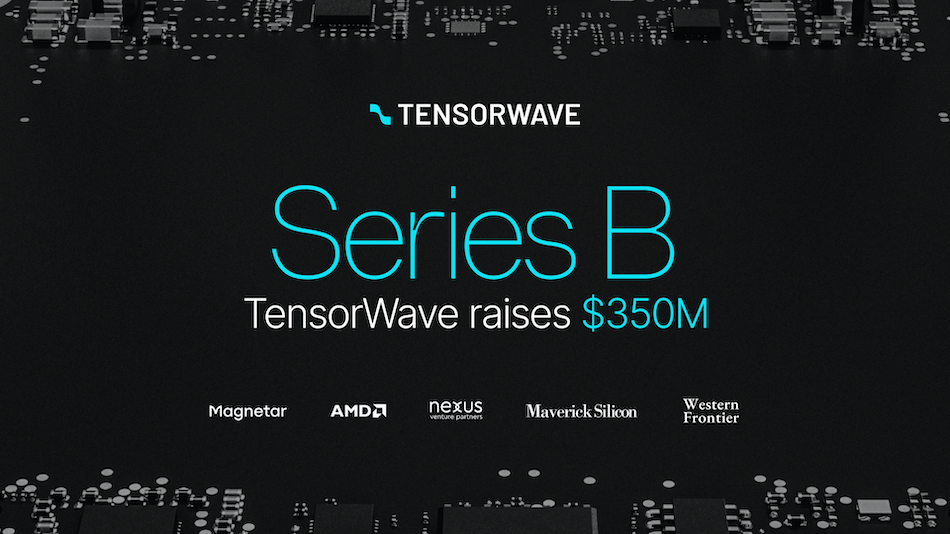

TensorWave Raises $350 Million Series B at $1.55B Valuation with AMD Ventures Co-Leading

The cleanest test in the market of whether AMD-only clouds work at scale.

TensorWave announced its $350M Series B on June 10 at $1.55B, co-led by Magnetar and AMD Ventures. The company runs one of the largest all-AMD clusters in North America: 8,192 MI325X GPUs online, MI355X queued, 2GW+ secured. Named customers include Fireworks AI and Luma AI.

Why this matters:

AMD Ventures co-leading is NVIDIA's playbook with CoreWeave, Nebius, and IREN: silicon vendor backs the cloud that runs its silicon exclusively. AMD's ecosystem play this month spans cloud (TensorWave), research (£2B UK, see Hardware), and hyperscale offtake (6GW Meta, Issue #93).

Fireworks and Luma running production inference on AMD is the multi-vendor proof point. If workloads stay, the diversification logic that pushed Anthropic to Broadcom and Microsoft to Maia becomes viable for tier-2 companies, not just frontier labs.

2GW of secured capacity puts TensorWave alongside CoreWeave, Lambda, and Nebius by footprint. AMD-exclusive is the differentiator. Long-term defensibility depends on AMD shipping MI355X and MI400 at competitive cost per token.

Era4 and Cosine Sign MoU to Build Lumen Sovereign on UK-Only Infrastructure

A UK frontier LLM paired with a UK infrastructure operator, a combination rarer than the press release suggests.

Era4 and Cosine signed an MoU on June 8 to develop Lumen Sovereign, one of the UK's first sovereign frontier LLMs trained entirely on UK-owned compute. Initial training runs on Isambard-AI. Cosine is in the first cohort of the UK Sovereign AI Fund. Era4 operates 40+ UK sites with land and power secured.

Why this matters:

The sovereignty claim deserves scrutiny. "No dependence on foreign infrastructure" means UK soil, UK operators, UK data residency. The GPUs inside Isambard-AI are NVIDIA GH200s, US-designed and Taiwan-fabricated. Under any model that includes silicon, this is intermediate-tier sovereignty. No one can claim better at current GPU economics.

Era4's 40+ UK sites matter more than the model. The UK has multiple model developers and Isambard-AI for training. The deployment layer at scale is what has been missing. Era4 is positioning there.

The MoU lands the same day as the £1.1 billion AI Hardware Plan and AMD's £2 billion commitment (see Hardware). Britain is backing the sovereign AI thesis at three layers in one week. Whether the stack integrates is the open question.

UK Commits £1.1 Billion to AI Hardware, AMD Commits £2 Billion to UK Research the Same Day

Two separate £1B+ commitments to UK AI hardware, announced six hours apart at the same conference.

The UK announced its £1.1 billion AI Hardware Plan at London Tech Week on June 8: £750 million for a national supercomputer including £150 million as an advance commitment to buy novel inference chips from UK startups this summer, plus a Playground Global UK fund backed by £150 million from the British Business Bank (its largest ever). AMD committed £2 billion over five years the same day to Imperial College, the Cambridge Zenith and Sunrise supercomputers, and Oriole Networks for the world's first large-scale AI system on a pure photonic network.

Why this matters:

The £150 million advance commitment applies the Operation Warp Speed model to silicon: state guarantees demand before chips ship, transferring market risk from startup to government. Fractile (Issue #105) and Olix are named beneficiaries. Britain is testing whether the model that funded early COVID vaccines also funds inference silicon.

AMD's £2 billion is structurally different from NVIDIA's UK presence: not GPU sales to operators, but five years of academic research and infrastructure. The Oriole photonic interconnect is the UK's bet that the network bottleneck (Issue #109 EE) gets solved with light, on AMD silicon.

Playground Global, led by former Intel CEO Pat Gelsinger, is opening its first non-US office in the UK. Britain has Arm, Fractile, Oriole, and a government writing the cheques. Whether the talent stays or gets acquired by US firms is the test of the next 24 months.

SpaceX IPOs at $75 Billion in Record Listing as Musk Outlines Terafab With Intel and ASML

The largest IPO in history priced on Thursday, listing a company that also operates the largest single AI training cluster on earth.

SpaceX raised $75 billion on June 12, the largest IPO ever recorded. Founder Elon Musk crossed $1 trillion in personal net worth. Musk addressed ASML's employee conference the same week to outline Terafab, a chipmaking plant with Intel and ASML to supply captive silicon for Tesla and SpaceX. Colossus, SpaceX's xAI-operated training cluster, already rents capacity to Anthropic at $1.25 billion a month (Issue #107). The IPO prices the compute revenue alongside the rockets for the first time.

Why this matters:

SpaceX is now structurally an AI hyperscaler. Colossus generates above $15 billion a year in contracted tenant revenue from Anthropic alone, before xAI workloads or any other tenant. A rocket company is generating compute revenue at the scale of a top-five public hyperscaler segment.

Terafab is the fifth non-NVIDIA silicon play in this issue and the most ambitious. The other four bet on alternative merchant vendors. Terafab bets on captive production for two specific customers, removing the merchant market entirely. Intel as foundry partner is the company that lost the hyperscaler CPU war becoming the manufacturing base for Musk's vertical integration.

The xAI-Tesla-SpaceX stack is structurally separate from every other AI infrastructure stack: xAI models on Colossus, SpaceX leasing capacity to outside tenants, Terafab silicon for Tesla and SpaceX. No NVIDIA. No Broadcom. No Apollo. The full stack from fab to training cluster to robotics now lives inside one ecosystem, opened to public capital on Thursday.

OpenAI in Talks to Lease 10GW Data Centre from SB Energy in Ohio

A single AI lab is negotiating to lease the operational equivalent of every Tier-1 UK data centre combined.

DCD reported on June 10 that OpenAI is in talks to lease a 10-gigawatt data centre from SB Energy, SoftBank's renewable energy arm, in Ohio. SB Energy has historically focused on US solar and battery storage. OpenAI's existing Stargate Michigan campus is 1GW.

Why this matters:

SB Energy moving from solar into data centre leasing is the next stage of energy/compute convergence. Microsoft buys fusion from Helion (Issue #109), Anthropic rents Colossus from SpaceX (Hyperscaler above), OpenAI may now lease from SoftBank's energy arm. The boundary between energy supplier, DC operator, and compute lessor is dissolving.

One lease, one customer, 10x the Stargate Michigan footprint. No single-tenant data centre commitment of comparable size exists in any market on record.

Ohio is positioning itself as the new Northern Virginia. AEP Ohio has been approving data centre interconnects at scale while PJM (Issue #107) and Minneapolis (Issue #108) constrain other markets. Whether the grid delivers 10GW to one customer in a useful timeframe is open.

The Rundown

The thread this week is divergence.

Two non-NVIDIA neoclouds in three issues, both backed by Blackstone. AMD's own venture arm doubling down on an AMD-only cloud. A government writing advance cheques for British inference silicon before chips ship. A trillionaire minted from a rocket company with an AI compute business bolted on the public market just priced.

The same week, SoftBank's $6 billion margin loan against the most valuable private AI company on earth could not close. The public market wrote $75 billion for SpaceX in days. Private credit wrote $35 billion for Apollo in days. The bilateral market could not write $6 billion for SoftBank in weeks. The market did not say no to OpenAI. It said no to concentrated, single-counterparty, privately-valued exposure.

This time last year, both OpenAI and NVIDIA were unassailable.

It’s amazing what can change in just 12 short months.

See you next week.